Bajaj Allianz Guarantee Assure Plan

Bajaj Allianz Guarantee Assure Plan Review

Bajaj Allianz Guarantee Assure plan is a traditional, non-participating, Endowment Assurance plan which provides the benefit of guarantee savings and insurance coverage.

Key Features

Benefits

When the plan matures, the benefit payable would be:

Basic Sum Assured + accumulated Guaranteed Additions

If the policy is taken on the life of a minor, the policy would mature only after the insured child attains 18 years of age irrespective of the tenure chosen.

If the insured dies during plan term, the death benefit would be:

Sum Assured on death + accumulated Guaranteed Additions till death

The Sum Assured on death would be higher of the following:

- Basic Sum Assured as chosen at policy commencement

- 5 times the annual premium

- 105% of all premiums paid until death

This value is paid if at least 1 full years’ premium has been paid by the policyholder who then asks for policy termination after 12 months of paying 1 year’s premium. Thus, this value would become payable 12 months after inception, revival or death. The value would be:

10% of premiums paid till date + 10% of Guaranteed Additions added

Bonuses are not declared under the plan.

Loan can be taken on the policy after the policy has acquired a Surrender Value. The maximum amount of loan available is 90% of the acquired Surrender Value.

Premiums paid under the plan would be exempt from tax under Section 80C up to a limit of Rs.1.5 lakhs. Premiums paid for the APC & CA option would be exempt under Section 80D. The death benefit or the maturity benefit received and the CI benefit if received would also be tax exempt under Section 10(10D) of the Income Tax Act.

No riders are available with the plan.

Any level of Sum Assured above the minimum level of Rs.1 lakh would attract a discount in the premium. The discount available would be Rs.7.50 per Rs.1000 Sum Assured.

A grace period of 30 days is allowed for payment of premium after the due date for annual, half-yearly or quarterly modes of premium payment. For monthly modes, the grace period allowed is 15 days. The life cover under the policy would continue during the grace period.

A cooling off period or a free look period of 15 days is granted to the policyholder after the policy issuance to review the policy terms and conditions. If found unsatisfactory, the plan can be cancelled within this period and the premium paid would be refunded after deducting the relevant mortality charge, service tax, cess and stamp duty paid.

Variants

Here is a specimen illustration showing the premiums payable at different levels of Sum Assured (SA),

term and age.

The tabulated rates are:

| Age | Term - 7 years | Term - 8 years | Term - 9 years | |||

| SA - 2 lakhs |

SA - 5 lakhs |

SA - 2 lakhs |

SA - 5 lakhs |

SA - 2 lakhs |

SA - 5 lakhs |

|

| 35 years | 47,028 | 116,445 | 49,214 | 121,910 | 51,744 | 128,235 |

| 40 years | 47,150 | 116,750 | 49,364 | 122,285 | 51,932 | 128,705 |

Non-Payment of premium in Bajaj Allianz Guarantee Assure Plan

Premiums have to be paid for at least 2 years after which the policyholder can surrender the policy or make it paid-up.

Making the policy Paid-up

If at least2 full years’ premium has been paid, the policy would become a paid-up policy if future premiums are not paid. The benefits under the plan would be reduced and would be called Paid-up benefits. Future Guaranteed Additions would not be declared under the policy and the following benefits would be paid as and when they occur:

- Death Benefit –Paid-up Sum Assured on death + accumulated Guaranteed Additions

- Maturity benefit – Paid-up Sum Assured + accumulated Guaranteed Additions

How it works

- The policyholder has to choose from an option of 3 plan terms of 7, 8 or 9 years.

- The premium would be limited to 5 years irrespective of the plan tenure chosen.

- Premium would be determined based on the Sum Assured and the policy tenure chosen by the policyholder.

- Guaranteed Additions @5% of the Sum Assured for a 7 year term, 6% of the Sum Assured for an 8 year term and 7% of the Sum Assured for a 9 year term would be added to the Sum Assured every policy year.

- On death during the period, the death benefit and accrued Guaranteed Additions is paid.

- On maturity, the maturity benefit and the accumulated Guaranteed Additions are paid.

- The policyholder or the nominee (in case of a death claim) can avail the maturity or the death benefit in monthly installments rather than as a lump sum over a period of 5 years or 10 years. The value of each installment would be calculated as follows:

For a 5 year benefit period – (1.04*Maturity/Death Benefit)/60

For a 10 year benefit period – (1.08*Maturity/Death Benefit)/120

These monthly installments can also be discontinued whereupon, the death or maturity benefit received would be:

Factor 3*Death or Maturity Benefit where, factor 3 would depend on the month of discontinuance

Plan Details

You can customize your policy to suit your requirement in the following manner:

Step 1: Choose your Sum Assured

Step 2: Choose your Policy Term (PT)

Your Premium will be based on your current age, Sum Assured, Policy Term

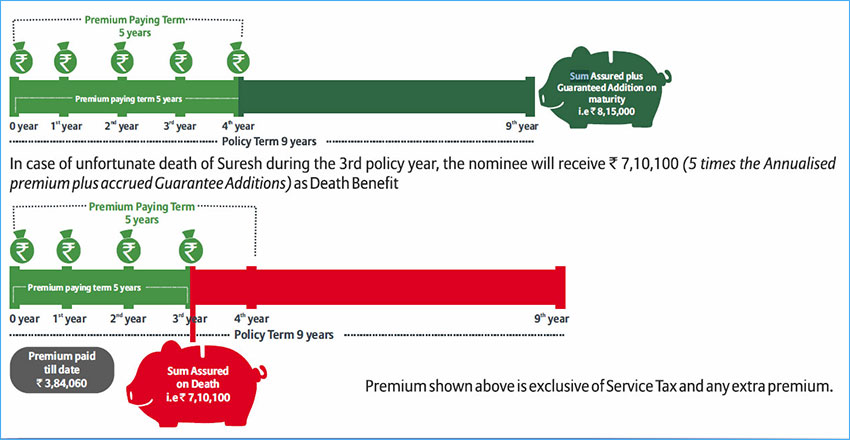

Let's Understand The Plan With An Example:

Suresh aged 30 years has taken a Bajaj Allianz Gurantee Assure poliy and opted and for a Policy Term (PY) of 9 years. The Sum Assured chosen by him is Rs.5,00,000 for which is is paying a premium of Rs.1,28,020 yearly. On maturity date, Suresh will receive Rs.5,00,000 (teh Sum Assured choosen) plus the accured Guranteed Addition of Rs.3,15,000.The maturity benefit received will be Rs.8,15,000.

Eligibility

The plan can be bought only by Resident Indians. The other eligibility criteria of the plan includes:

| Minimum | Maximum | |

| Entry age (Last Birthday) | 9 years | 60 years |

| Maturity Age (Last Birthday) | 18 years | 69 years |

| Plan tenure | 7, 8 or 9 years | |

| Premium payable | Yearly – Rs.23,839 Half-yearly – Rs.12,158 Quarterly – Rs.6198 Monthly – Rs.2145 |

No limit. Depends on the Sum Assured chosen |

| Premium Paying Term | 5 years | |

| Sum Assured | Rs.1 lakh | No limit |

| Premium payment mode | Monthly, quarterly, half-yearly and annually or Single Premium | |

Surrender Value

Surrender is allowed only after the policy becomes paid-up, i.e. after 2 full years’ premiums have been paid. On surrendering the policy, higher of the Guaranteed Surrender Value (GSV) or the Special Surrender Value (SSV) would be paid.

- GSV = (Basic Premium paid excluding taxes * GSV Factor)+ (Accumulated Guaranteed Additions* GSV factors of such additions)

- The SSV would be declared by the company based on its performance

Revival is allowed within 2 years from the date of the first unpaid premium. The policyholder would be required to pay the outstanding premium and any interest charged by the insurer to revive his policy.

If a loan is availed under a policy, the loan and the interest therein should not exceed the Surrender Value in the policy. If the policy is in-force, this does not happen. If the policy is made paid-up, the policyholder would be notified and the policy would be foreclosed.

Exclusions

- If the policyholder commits suicide within a year of policy issuance 80% of the premiums paid would be returned and no death benefit would be payable.

- If suicide is committed within a year of policy revival, higher of 80% of the premiums paid till death or the Surrender Value acquired would be paid provided the policy is in force.